Becoming a first-time homeowner comes with many new experiences, from getting approved for a mortgage to reviewing and signing closing documents. One of the most important parts of buying a home is obtaining insurance to help protect you and your new investment. If you’re looking for homeowners insurance for the first time, you may wonder where to begin.

The right policy offers tailored protection for Pennsylvania’s specific weather risks, from harsh winter storms to strong winds. Our guide and checklist can help you break this process down into steps and secure the coverage you need.

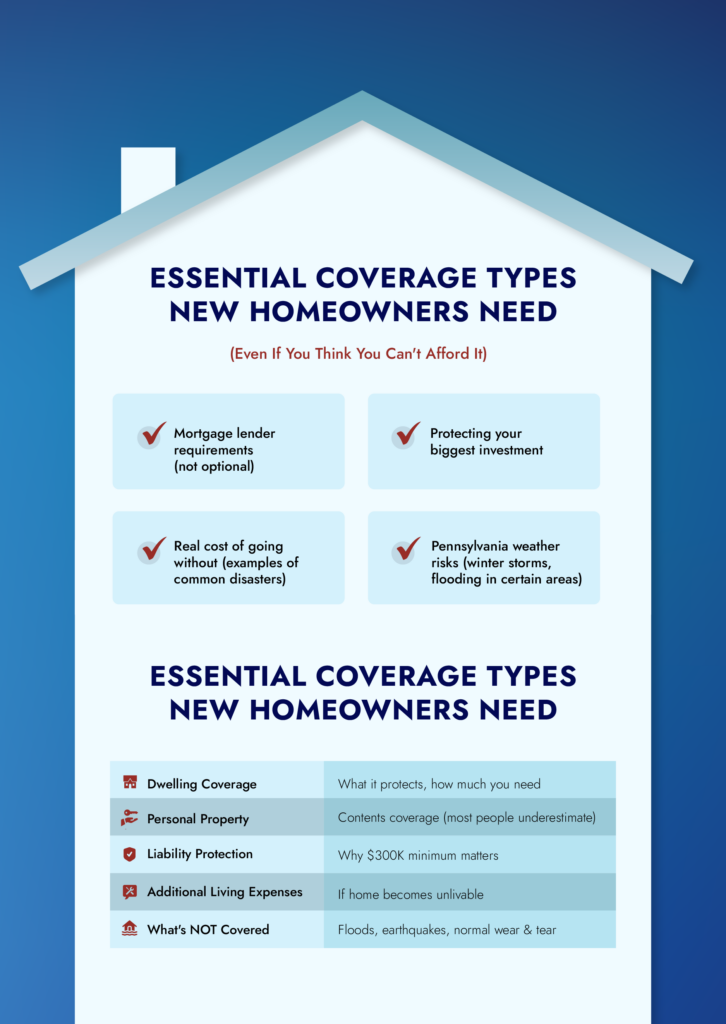

Why Homeowners Insurance Matters (Even If You Think You Can’t Afford It)

As you consider the significant investment you’ll need to make in your home, you may question whether you can skip the homeowners insurance and save money. While homeowners insurance isn’t required by law, mortgage lenders will only fund your loan if you have it.

Homeowners insurance also provides the ultimate safeguard for your most significant investment. Without coverage, you could experience high out-of-pocket costs for damage to your home or its contents. In Pennsylvania, you may face specific weather risks, like blizzards and severe windstorms.

Essential Coverage Types New Homeowners Need

If you’re wondering what insurance you need for a new house, here are the main types of coverage typically included in homeowners insurance policies:

- Dwelling coverage: This coverage protects the home’s physical structure. The homeowners insurance you need in Pennsylvania depends on the home, but you should focus on full replacement cost rather than the home’s market value.

- Personal property: With this coverage, you can protect all your personal belongings from covered perils, even when they are away from your home. Focus on correctly estimating the value of your furniture, electronics, clothing and other belongings to get sufficient protection.

- Liability protection: If someone suffers injury on your property, or you accidentally damage another person’s property, this solution may help cover medical bills, repair costs and legal fees. Having a liability limit of at least $300,000 is recommended, though a higher limit may be ideal depending on your situation or level of risk.

- Additional living expenses: Also called loss of use coverage, this solution can help cover hotel stays, meals and other necessary expenses if a covered disaster temporarily makes the home uninhabitable.

While homeowners insurance offers significant coverage, most standard policies exclude floods, earthquakes and normal wear and tear. If you would like coverage for these situations, you will need to discuss specialty add-ons with an insurance advisor.

The New Homeowner Timeline

Buying a home comes with many responsibilities, including obtaining homeowners insurance. Follow this homeowners insurance checklist to stay on track.

Before Closing

About 30 days before closing on your new home, you should take the following steps:

- Get quotes from about three to five carriers. Ask an independent broker to shop the market for you to find the best solutions.

- Compare the quotes to determine the actual value of the coverage you receive, rather than just the bottom-line price.

- Explore how different deductible options impact your monthly premium.

- Ask your advisor about specific discounts you can access as a new homeowner or by installing particular safety features.

Week of Closing

On the week of closing, you’ll need to:

- Confirm that the policy is scheduled to activate on the exact closing date.

- Submit proof of insurance documents to your mortgage lender.

- Take photos and videos to document the home’s initial condition for your records.

- Save your independent agent’s contact information in your phone for simplified emergency access.

First 30 Days

During your first month of home ownership, you should:

- Inventory all your personal belongings, room by room.

- Install or upgrade smoke and carbon monoxide detectors to maximize safety and qualify for potential policy discounts.

- Test your home security system.

- Review finalized policy documents thoroughly with your insurance advisor.

- Discuss bundling your new home policy with your auto insurance for maximum value.

Ongoing Maintenance

As you settle into your home, here are a few tasks to complete regularly or as needed:

- Commit to an annual policy review with your agent to ensure your coverage is up to date.

- Update your coverage limits immediately following any major home renovations or additions.

- Report significant lifestyle changes that may impact your policy.

- Recalculate your home’s replacement cost annually to keep pace with inflation and building costs.

Common First-Time Buyer Mistakes (And How to Avoid Them)

Knowing how to avoid pitfalls when choosing a policy can save you time and money in the long run. Here are a few common mistakes people make with first-time home buyer insurance:

- Only shopping by price: Cheap policies can leave gaps, which may be costly in the event of a claim. Focus on overall value.

- Underestimating replacement cost: Instead of insuring based on the real estate market, consider the actual cost of construction materials and labor.

- Not documenting belongings: An inventory streamlines the process of personal property claims.

- Skipping umbrella coverage: If you want high-limit liability protection that extends beyond standard policies, umbrella coverage is the solution.

- Waiting until the last minute: Delaying insurance shopping can push back your closing date and limit insurance options.

- Not asking about discounts: Independent advisors actively seek ways to save you money without sacrificing protection.

Check Insurance off Your Closing To-Do List

If you need help with the homeowners insurance process, AAdvantage Insurance Group can support you. As local, independent advisors, we shop multiple trusted carriers to secure the rock-solid coverage you need. Contact us before your closing date for a personalized quote.